Entropy and Mutual

Information

Let:

-

X be a random variable (R.V).

-

P(X) be the probability distribution of X.

-

p(x) be the probability density of X.

The entropy of X, H(X) is defined by:

H(X) = -EX[ log(P(X)) ]

Entropy is a measure of randomness. The more random a variable is, the more entropy it

will have.

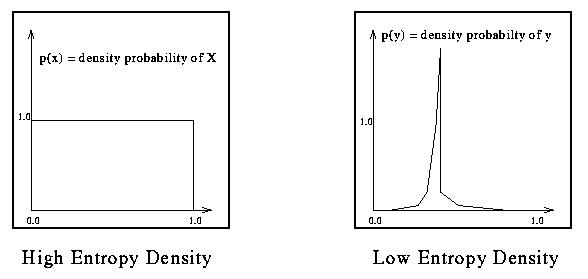

Example:

The joint entropy is a statistics that summarizes the degree of dependence of a RV X

on an other RV Y. It is defined by:

The joint entropy is a statistics that summarizes the degree of dependence of a RV X

on an other RV Y. It is defined by:

H(X,Y) = -EX [EY [ log(P(X,Y)) ] ]

The conditional entropy is a statistics that summarizes the

randomness of Y given knowledge of X. It is defined by:

H(Y|X) = -EX [EY [ log(P(Y|X)) ] ]

Two random variables are considered to be independent if:

H(X,Y) = H(X) + H(Y)

The Mutual Information, MI, between two random variables X and Y is given by:

MI(X,Y) = H(Y) - H(Y|X) = H(X) + H(Y) - H(X,Y)

(It's thus a measure of the reduction of the entropy of Y given X.)